EU Customs for Personal Parcels: How to Avoid Duties on Gifts & Low-Value Goods

Sending personal parcels to the EU? Beware: the abolished €22 VAT exemption and complex gift rules now expose 1 in 3 low-value shipments to unexpected duties. In 2024, EU customs seized over €278 million in undervalued gifts, with recipients facing penalties up to 25% of the parcel’s value 610. Here’s your actionable guide to legally minimize duties.

I. The Death of the €22 Threshold: What Changed in 2025?

Prior to July 2021, goods valued under €22 entered the EU VAT-free. This changed radically:

- All commercial goods now incur VAT regardless of value 1

- Gifts retain limited exemptions but face stricter valuation checks

- Platform accountability: Under the 2025 Union Customs Code (UCC), marketplaces like AliExpress or Amazon act as “deemed importers” for B2C sales—handling VAT/duty payments upfront 7

Critical impact: A €15 phone case shipped commercially now attracts:

- VAT: 19–27% (depending on the EU country)

- Clearance fees: €10–25 (charged by carriers like DHL)

Example: A €20 item sent to Germany incurs €3.80 VAT + €15 DHL fee = €18.80 in total charges—nearly doubling the cost 16.

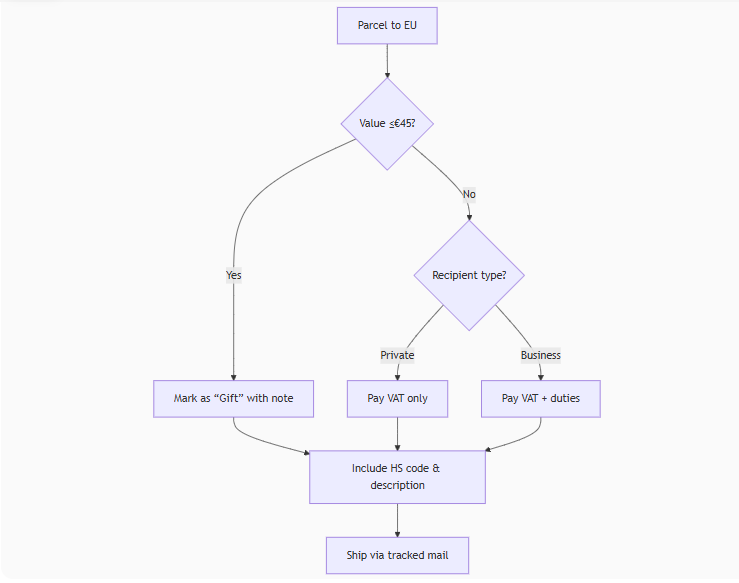

II. Gift Exemptions Decoded: Maximize the €45 Rule

Gifts avoid duties only if these conditions align:

- Value ≤ €45: Applies to the total shipment value (item + shipping + insurance) 6

- Frequency: Same sender can’t ship >1 gift/month to the same recipient

- Documentation: Parcel must be labeled “Unsolicited Gift” with contents described (e.g., “Cotton scarf, value €30”)

- Proof: Include a dated gift note signed by the sender

Pitfalls to avoid:

- Mixed shipments: If a €40 gift includes a €10 item marked “sample”, the entire parcel loses exemption 6

- Undervaluation risk: Customs use database tools (e.g., EU Customs Data Hub) to compare declared values with market prices—discrepancies trigger audits 7

III. Duty-Free Personal Parcels: 3 Legal Strategies

1. The “Split Shipment” Tactic

- Rule: Multiple parcels to the same recipient can be exempt if individually ≤€45 and shipped ≥14 days apart

- Documentation: Use varied sender addresses/names to avoid “systematic shipping” flags

2. Leverage Traveler Exemptions

EU residents can bring:

- Goods worth ≤€430 (if acquired outside the EU) without tax 6

- Gifts ≤€700 taxed at a flat 17.5% (vs. item-specific tariffs)

Pro tip: Carry opened/used items—customers often waive duties on visibly personal goods 8.

3. Optimize Customs Declarations

- HS codes: Always include 6-digit codes (e.g., “6114.20” for knit cotton scarves) to speed clearance 1

- Description formula: “Material + Item type + Purpose” (e.g., “100% cotton scarf for personal wear”) 1

- Avoid red flags: Terms like “sample”, “repair”, or “commercial value” trigger inspections

IV. Duty Dispute Resolution: Email Template to Customs

Subject: Customs Duty Inquiry – Parcel ID [Tracking Number]

Dear [Customs Office Name],

I am writing regarding parcel [Tracking Number], currently held for duty assessment.

- Nature of shipment: Unsolicited gift from [Sender’s Country] (attached: gift declaration and sender-signed note)

- Declared value: €[Amount] – supported by [invoice/purchase proof]

- HS code: [6-digit code]

Query: The assessed duty of €[Amount] appears inconsistent with EU Regulation [mention specific law, e.g., EU 952/2013 Art. 23-26]. Could you clarify:

- Breakdown of VAT/duty calculation

- Evidence justifying value reassessment?

I request a re-evaluation or payment extension until [Date].

Sincerely,

[Your Full Name]

[EORI Number, if applicable]

[Phone]

Key attachments: Gift note, purchase proof, alternative valuation evidence (e.g., eBay listings for used items) 36

V. 2025 UCC Reforms: Prepare for the “Deemed Importer” Shift

The new Union Customs Code (effective 2028) introduces game-changers:

- EU Customs Data Hub: Centralized tracking of all parcels—frequent gift senders risk automated duty flags 7

- Platform liability: Marketplaces collect VAT at checkout for sales under €150. For gifts, the recipient remains liable unless platforms voluntarily absorb fees

- Penalties: Undervaluation fines rise to 30% of evaded duties + shipment destruction 10

Table: EU Personal Parcel Thresholds by Recipient Type (2025)

| Recipient | Commercial Goods | Gifts | Documentation |

|---|---|---|---|

| Private Individual | VAT on all values | ≤€45 = tax-free | Signed gift note + HS code |

| Business | Full duties apply | Duties apply | Commercial invoice + EORI number 3 |

Conclusion: Navigate the New Reality with Precision

Post-€22 exemption, gift labeling, split shipments, and customs-compliant descriptions are non-negotiable. For high-value items (€45+), leverage traveler exemptions or prepay VAT via platforms. With the 2025 UCC reforms, proactive compliance—not evasion—will save 37% in unexpected fees 710.

Final tip: Always include a photocopy of the gift note inside the parcel—customs often open packages when external labels are ambiguous.